Milestone registrations to expedite Hot Chili copper-gold project

Doug Bright BULLS N’ BEARS

Hot Chili has secured the milestone government registrations necessary to help fast-track its Costa Fuego copper-gold and Huasco Water projects in Chile.

The registrations, before Chile’s Office for Sustainable Project Management, confirm the two projects meet the government’s key criteria for consideration for a list of strategic investment projects that could be prioritised through a streamlined administrative approvals process.

Part of the office’s objectives is to optimise and accelerate approvals for projects that promote sustainability.

Hot Chili’s maiden combined probable open pit and underground ore reserves for its Costa Fuego project stands at 502 million tonnes at 0.37 per cent copper, 0.10 grams per tonne (g/t) gold, 0.49g/t silver and 97 parts per million molybdenum across multiple processing streams. The streams include the sulphide concentrator, oxide leach and low-grade sulphide leach processes.

The total combined metal in the reserves is a heady 1.86Mt copper, 1.58M ounces of gold, 7.95M ounces silver and 49,000t molybdenum.

Significant additional opportunity exists to extend the overall resource numbers with the company’s recent discovery of copper-gold porphyry mineralisation at its non-contiguous but nearby La Verde project.

La Verde is the latest addition to Hot Chili’s Costa Fuego production hub. It is only 50 kilometres south by road from the company’s central processing facility at Productora, within the company’s Costa Fuego group of projects.

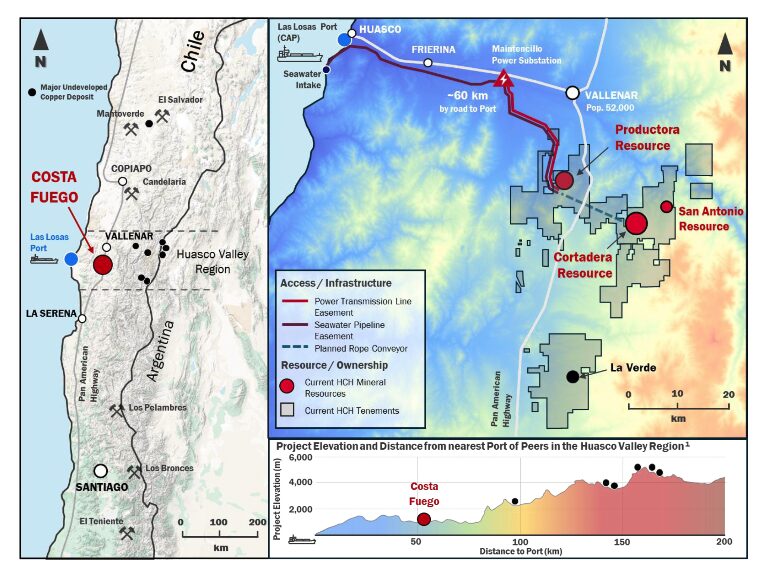

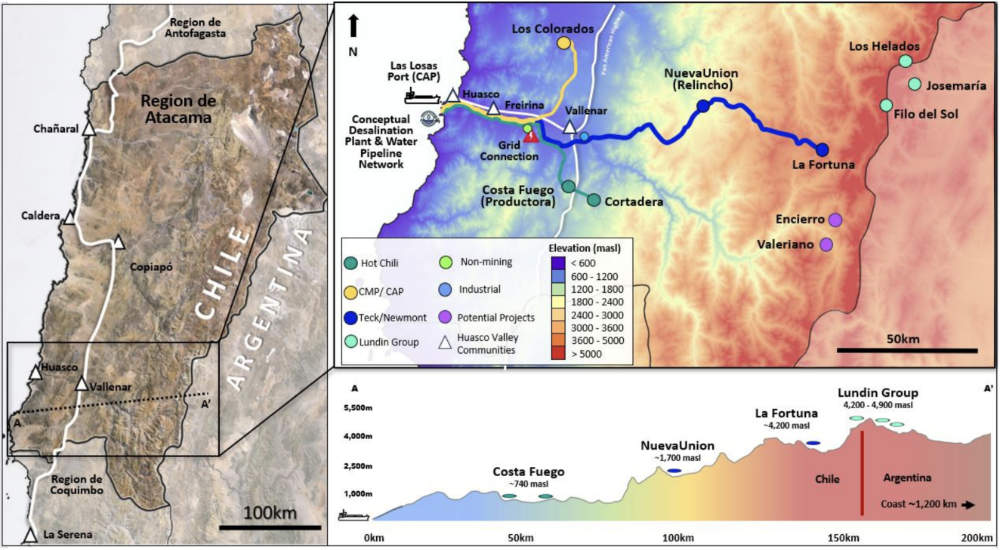

The Costa Fuego complex is on Chile’s coastal range and comprises the company’s principal reserves zones at Productora, Alice, San Antonio and Cortadera, which all lie within a radius of about 10km.

The centre of the company’s contiguous tenure and its current resources is about 63km southeast of the port city of Huasco, in the Huasco province of the nation’s highly prospective Atacama region.

Huasco plays an important role in Hot Chili’s plans, as it is the proposed location for the seawater intake for the company’s Huasco Water project.

Huasco Water is an joint venture between Hot Chili and Chilean mining company Compañia Minera Del Pacifico. With its first-mover advantage, Huasco Water is the only company permitted to supply seawater in the Huasco Valley region, following a 10-year regulatory approval process.

The combined projects possess a valuable, unique and strategic mix for Hot Chili over the next decade and have what the company describes as a “top quartile copper production capacity with lowest quartile capital intensity”.

Hot Chili undertook March pre-feasibility studies for the water and the Costa Fuego gold-copper projects. A positive study outcome provides Hot Chili with an opportunity to consider the strategic value of its 80%-owned subsidiary company Huasco Water, which controls all its critical water assets.

The company sees significant value potential in outsourcing its vital seawater supply infrastructure and has secured Huasco Water’s position by executing a memorandum of understanding for a ground-breaking seawater offtake agreement for a proposed large-scale, multi-customer water business.

Its stage one water supply pre-feasibility study examined the delivery of 500 litres per second (L/s) of seawater, followed by a stage two 1300L/s of desalinated seawater supply.

A conceptual stage three study looked at future expansion to supply up to 2300L/s of desalinated water.

The staged approach considers the initial establishment of seawater supply infrastructure, including pumps and pipelines, towards the end of the decade, to be followed by an initial desalinated water supply and then subsequent phases of expansion.

It would enable long-term water supply to be scaled to regional demand growth to support mining, communities and agriculture in the Huasco Valley, with the potential to extend well beyond the project’s initial horizons.

The concept is further supported by significant interest in Huasco Water displayed by other Chilean and international water infrastructure investment groups, along with nearby mine developers, agricultural and community groups and government bodies.

Hot Chili says while long permitting timelines continue, its desalination permitting is progressing and no regulatory changes have been made to Chile’s maritime permitting process since Huasco Water was granted its concession.

Additionally, the company’s environmental impact assessment (EIA) is advancing, with its stage one seawater supply baseline studies completed for inclusion in its Costa Fuego EIA.

The latest registration is a significant milestone that confirms Hot Chili’s projects meet the Chilean government’s objective criteria to acquire priority status.

With the paperwork in hand for both Costa Fuego and Huasco Water, the company is now able to centralise and monitor all of its active permitting processes through a single platform and supervisory entity.

The current permitting needs include the company’s second maritime concession application for Huasco Water and its upcoming EIA submission for Costa Fuego and Huasco Water.

Hot Chili doubles copper-gold discovery footprint in Chile

STOCKHEAD

- HCH doubles footprint of La Verde copper-gold discovery

- Prospect sits within Costa Fuego project in Chile’s Atacama region

- Company planning deeper drilling to expand discovery further

Special Report: Hot Chili has doubled its porphyry discovery footprint at its Chilean project, with a third round of strong assay results at the La Verde copper-gold discovery at its Costa Fuego project.

La Verde is around 30km south of the Costa Fuego planned central processing hub at low elevation in the coastal range of the Atacama region.

The phase one reverse circulation (RC) drilling has now doubled the initial discovery footprint, confirming copper-gold mineralisation extends over 1km in length and up to 750m in width, from near surface.

Notable results include:

- 389m grading 0.4% copper and 0.1g/t gold from 4 m depth to end-of-hole (DKP030), including 46m at 0.6% copper and 0.2g/t gold from 238m, including 34m at 0.6% copper and 0.2g/t gold from 322m;

- 120m grading 0.4% copper and 0.1 /t gold from 6m depth (DKP028), including 48m at 0.5% copper and 0.1g/t gold from 26m and, 114m at 0.3% copper, 0.1g/t gold from 318m depth to end-of-hole, including 34m at 0.4% copper, 0.2g/t gold from 380m to end-of-hole;

- 114m grading 0.4% copper from 86m depth (DKP024), including 52m at 0.5% copper and 0.1 g/t gold from 96m;

- 286m grading 0.3% copper and 0.1g/t gold from 4m depth (DKP027), including 154m at 0.4% copper, 0.1g/t gold from 44m; and

- 228m grading 0.3% copper and 0.2g/t gold from 42m depth (DKP013), including 104m at 0.4% copper and 0.3g/t gold from 42m.

Hot Chili (ASX:HCH) has also confirmed higher-grade centres across the extent of the shallow oxide and sulphide discovery, indicating:

Importantly, multiple distinct higher-grade centres have been confirmed from near surface. Assessment of each of these higher-grade centres indicates:

- A North-East (NE) higher-grade centre, 180m strike by 280m width by 320m in vertical extent

- South-east (SE) higher-grade centre, 320m strike by 340m width by 400m in vertical extent

- South-west (SW) higher-grade centre, 90m strike by 120m width by 260m in vertical extent

Deeper diamond drilling planned

Since over half of the drill holes ending in significant mineralisation at the limit of RC drilling depth capability, HCH is on the hunt for a potentially larger porphyry cluster at La Verde.

The extent of the mineralisation beneath the open pit remains untested.

The company is now planning deeper diamond drilling for phase two to extend these higher-grade centres at depth.

This could potentially add to the open-pit mine life for the Costa Fuego hub, with further development study updates expected in the near-term.

Watch: Hot Chili adds mine-making credentials for Costa Fuego copper-gold

Regulatory application for phase-two drilling access is progressing, with drilling to commence once approved.

In the meantime, development study activities to optimise the recent Costa Fuego Pre-Feasibility Study (PFS) are underway, building on the recently released PFS, which highlighted impressive post-tax numbers for the asset including an NPV of US$1.2b and IRR of 19%.

All-in sustaining costs totalled US$1.85/lb from the production of 1.5Mt of copper and 780,000oz of gold over a 20-year mine life.

The Copper Play the Market Is Missing

Streetwise

Disconnects between price and value in the resource sector occur regularly but are usually accompanied by issues. Issues such as a low metal price, local social pressures, political interference, or an environmental problem.

In situations like these, the disconnect between price and value makes sense. There is something that has to be overcome to get price recognition from the market. Investors looking to take positions in these sorts of situations must be cautious of their approach and understand how these risks will be overcome. In essence, this is what a contrarian investor is all about: taking a calculated risk on a solution to issues such as these.

That said, there are times when there is a disconnect and no major reason for it. These aren’t as common, but I have learned that when I personally come across them, I need to pursue them as strongly as I can. These are the true asymmetrical bets that can really propel a portfolio’s return forward.

Over the last two years, I have personally benefited by identifying a few of these situations, taking a big position, and waiting.

In my experience, the biggest factor to overcome in situations is time.

As they say, patience is a virtue. In situations like this, it becomes glaringly obvious.

Today, I have for you an opportunity that I think has no obvious reason for the major disconnect between price and value. The company is focused on developing two copper-gold porphyry projects in Chile. One is at the feasibility study stage, while the other is a brand new discovery story.

The company is

Hot Chili Ltd. (HCH:ASX; HCH:TSXV; HHLKF:OTCQX).

Let me explain to you why I think this is arguably the most undervalued junior mining company in the sector right now.

Costa Fuego

Costa Fuego is Hot Chili’s flagship project, which just recently had a PFS completed.

Costa Fuego will be both an open pit and an underground mining operation in the future.

On average, it will produce 116kt CuEq (copper equivalent) for 14 of the 20 years of its mine life, making it one of the largest undeveloped copper operations owned by a junior.

In terms of economics, Costa Fuego has great leverage to the copper price, with an NPV above US$2B and an IRR of 27% at US$5.30/lb copper.

- Post-tax NPV8% of US$1.2 B and IRR of 19% (at US$4.30/lb copper)

- Post-tax NPV8% of US$2.2 B and IRR of 27% (at US$5.30/lb copper)

As I mentioned, Costa Fuego will start as an open pit mining operation and then transition to an underground block caving operation later in the mine life.

Upfront CAPEX is, therefore, estimated to be US$1.27B with an expansionary capital around US$1.35B — big mines cost big money.

If I were to pick a reason for Hot Chili’s low valuation, this might be it. That said, if you look at all of the large, advanced (at least PFS level) projects out there and owned by a junior, billions in CAPEX is the commonality.

Not only this, but I view Hot Chili’s recent discovery of copper-gold mineralization at their La Verde project as reason to believe that the impact of the CAPEX will be lessened.

Discovery hole: DKP002 308m of 0.5% copper + 0.3g/t gold, including 202m of 0.6% copper + 0.3g/t gold, and including 100m of 0.7% copper + 0.3g/t gold.

As I see it, La Verde has the potential to add significant amounts of ore early on into a future combined mining operation. This additional open pit tonnage from La Verde could be trucked to nearby Costa Fuego and push out the expansionary capital needed to build the underground — this is very meaningful.

In a discounted cash flow model, cash flows in the future are discounted.

Meaning, the earlier in a mine life you can produce higher cash flow, the better the net present value (NPV).

Hot Chili still has much to prove at La Verde, but I think they are well on their way to doing it.

In closing, additional tonnage from La Verde doesn’t negate the size of the CAPEX; what it does is push it further out in the mine life, which will increase the overall NPV of the project.

Huasco Water

One of the biggest factors affecting copper project development in both Chile and Argentina right now is access to water. On the Chilean side, it’s both an altitude and a permit issue.

Firstly, the Chilean government is no longer allowing water extraction via underground sources. They are exclusively forcing development projects to apply for a maritime concession or do a deal with a company that already has one. A maritime concession allows for the extraction and treatment of seawater.

The reality of the situation is that there have only been two maritime concessions granted in the last 13 years. One of those was granted to Hot Chili, which has since placed that permit into Huasco Water — of which they own 80%.

Hot Chili is now very much in the driver’s seat for water supply of a region which is on the cusp of a major development cycle.

Now, I don’t believe that this situation allows Hot Chili to unreasonably leverage their position; that isn’t what the Chilean government would promote or accept.

What it means, though, is that HCH has a major source of value that the market isn’t giving them credit for.

So the question begs: What are the water rights worth?

It’s a great question, one that I can’t fully answer.

What I will draw your attention to is Antofastga’s deal with Transelec and Almar Water Solutions for $600M. That situation is a little different because it includes some existing infrastructure, but essentially gives us a rough idea of what these types of assets are worth.

Further, Hot Chili completed an economic study on the Huasco Water business, which proves its potential — 2 Stage / 1300L/s Desalinated Water Supply: Post-tax NPV(8%) of US$977M and IRR of 19%.

Not only do I think that this supply is meaningful for Chilean development projects, but it is an obvious source of water for the Argentinian side, too.

I think one of the biggest misnomers right now is the water situation for a few of the largest copper development projects in the world — BHP & Lundin’s Jose Maria and Filo projects.

Personally, I don’t think they have an alternative to doing an off-take agreement with Hot Chili’s Huasco Water. . .

Concluding Remarks

Nothing is for sure in life, especially in the junior mining sector. However, once in a while there are asymmetric bets that you can make that are mostly a function of time, rather than the solving of some other specific issue.

In my view, the opportunity in Hot Chili is one of those high-potential asymmetric bets whose value recognition is just a matter of time.

Currently, Hot Chili’s MCAP is around $70M, which I think is extremely cheap.

Its flagship project, Costa Fuego, has a PFS completed on it with an after-tax value well over US$1B at today’s copper price. Not only is the project undervalued to the current state of development, but I think it has a clear path towards optimization with the combination of the discovery at La Verde.

The real X-Factor lies with Huasco Water, which holds the water rights to a region of Chile and Argentina which is on the cusp of major development.

Mine construction and operation don’t happen without water, and, therefore, this is a catalyst that is very much a when question, not if.

With over AU$10M in cash, continued drilling at La Verde and the potential for water offtake agreements to be signed with Huasco, I believe it is only a matter of time before Hot Chili’s value is recognized by the market.

Hot Chili strengthens team to push Chile projects into development

Andrew Todd BULLS N’ BEARS

Hot Chili has secured the services of two seasoned mining executives to bolster leadership as the company progresses its Costa Fuego copper-gold project and Huasco Water venture in Chile’s Atacama region.

Ex-Gold Fields Australia executive Stuart Mathews joins as non-executive chairman, while Chilean copper expert Alberto Cerda assumes the role of project director. Cerda brings a particular set of skills… namely in mine development and operations to support the company’s upcoming definitive feasibility studies for both projects.

The appointments align with Hot Chili’s strategic focus on advancing its low-altitude, copper and water projects amid a looming copper market, which has international majors clamouring for quality.

Hot Chili says Mathews’ and Cerda’s proven expertise in delivering large-scale mining operations – particularly in Chile in Cerda’s case – positions the company to navigate the complexities of project development, resource optimisation and strategic partnerships in the world’s top copper producing country.

Costa Fuego is a large copper-gold porphyry set to churn out 116,000 tonnes per annum of copper-equivalent metal, which includes 95,000t of copper and 48,000 ounces of gold in its first 14 years. Importantly for Hot Chili’s metals mix, chairman Mathews comes from a gold mining background as the recent executive vice president for Gold Fields in Australasia, where he oversaw operations producing more than 1 million ounces of gold annually.

Cerda takes care of the copper background as a Chilean mining engineer with more than 40 years of experience in major copper projects in Chile for companies such as Newmont, Barrick and BHP Billiton.

Hot Chili’s projects are strategically positioned to benefit from rising copper demand and regional infrastructure needs. Costa Fuego’s robust economics and Huasco Water’s exclusive water supply permit make it strategically significant to the region.

With environmental permitting and exploration ongoing, the company is well-placed to deliver and further extend its overall resource numbers, thanks to a recent discovery of copper-gold porphyry mineralisation at its non-contiguous but nearby La Verde project.

Located 60 kilometres from Las Losas port on Chile’s coastal range, Costa Fuego is Hot Chili’s flagship project. A recent prefeasibility study outlined a 20-year mine life with a maiden ore reserve of 502Mt grading 0.37 per cent copper, 0.10 grams per tonne (g/t) gold, 0.49g/t silver, and 97 parts per million (ppm) molybdenum, with a contained 1.86Mt copper, 1.58M ounces gold, 7.95M ounces silver and 49,000t molybdenum.

The project is expected to generate a post-tax net present value (NPV) of US$1.2 billion at a US$4.30 a pound copper price and US$2280 per ounce gold price. At current market prices, the NPV increases to US$2.2B, with a 19 per cent internal rate of return and a five-year payback on US$1.27B capital expenditure.

Hot Chili’s 80 per cent-owned Huasco Water project, in partnership with Compañia Minera del Pacifico, addresses critical water scarcity in the Huasco Valley.

Secured after a decade-long regulatory process, Huasco Water holds the region’s only maritime licence for seawater supply, providing the project with a significant competitive advantage. Its recent pre-feasibility study detailed a two-stage development plan to supply water to local major copper producers, to earn an estimated revenue of US$9.35B and a US$977M NPV over 22 years of supply.

The company has completed its baseline environmental studies and a second maritime concession application is under review, positioning Huasco Water, like Costa Fuego copper, to commence supply by the end of the decade.

With copper prices soaring and gold continuing at all-time highs, the appointments come at pivotal time in the company’s development. Hot Chili says it remains on a tidy $7.5M cash pile to rapidly expand its resources, while simultaneously courting strategic partners for production at its huge copper and water undertakings.

Hot Chili rocks out as drilling reveals potential scale of “major” La Verde copper-gold discovery

February 11, 2025 | Stockhead

- Hot Chili drilling intersects more broad zones of copper-gold mineralisation at La Verde

- Results highlight potential to be the company’s next major copper-gold discovery

- Assays pending for a further seven holes while step-out drilling is underway

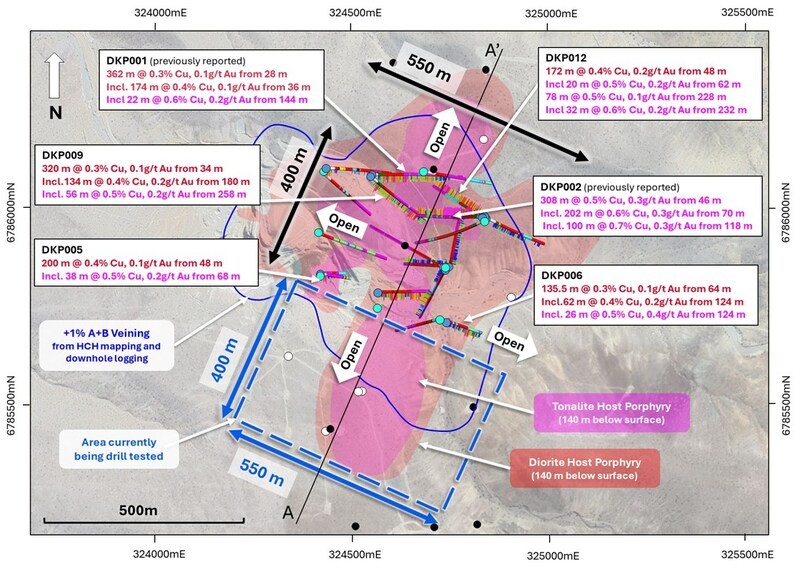

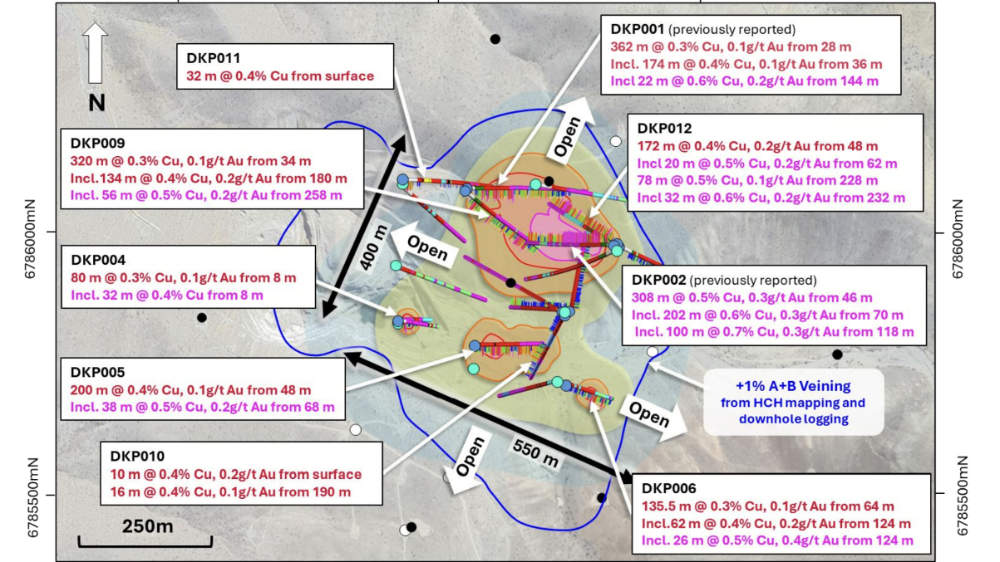

Special Report: Hot Chili now has multiple new significant drill intersections from a further 10 holes to prove that its La Verde project in low elevation coastal Chile is a major copper-gold porphyry discovery.

The company first received a taste of the project’s potential back in mid-December 2024 after announcing very thick copper-gold intersections from its first two drill holes.

Hole DKP001 got the show on the road with a 174m intersection grading 0.4% copper and 0.1g/t gold from a down-hole depth of just 36m before DKP002 quickly blew Hot Chili’s (ASX:HCH) expectations out of the water with a stunning 308m interval at 0.5% copper and 0.3g/t gold from 46m to end of hole.

DPK002 also hosts a higher grade zone of 202m at 0.6% copper and 0.3g/t gold from 70m, which is encouraging from a development standpoint as its places the richest resources closer to surface.

A fantastic start no matter how you look at it and one that just got a whole lot better.

Assays from another 10 holes have now returned broad, consistently mineralised intersections extending over 300m vertically that start from shallow depths.

Notable intersections from the rapidly growing oxide and sulphide find are:

- 320m at 0.3% copper and 0.1g/t gold from 34m to EOH including 134m at 0.4% copper and 0.2g/t gold from 180m and 56m at 0.5% copper and 0.2g/t gold from 258m (DKP009)

- 200m at 0.4% copper and 0.1g/t gold from 48m to EOH including 38m at 0.5% copper and 0.2g/t gold from 68m (DKP005); and

- 172m at 0.4% copper and 0.2g/t gold from 48m including 20m at 0.5% copper and 0.2g/t gold from 62m with a separate intersection of 78m at 0.5% copper and 0.1g/t gold from 228m to EOH including 32m at 0.6% copper and 0.2g/t gold from 232m (DKP012).

Major discovery

The new drill results outline La Verde’s potential scale with managing director Christian Easterday saying the project is shaping up to be the company’s next major copper-gold discovery that could lift the scale of its Costa Fuego project.

“With primary copper supply declining, copper and gold prices rallying, and a PFS on each of our planned businesses (copper-gold and water) nearing completion – momentum is building fast,” Easterday said.

“Following in the footsteps of our successes at Cortadera and Productora, we’ve secured full control of La Verde after years of strategic consolidation, finally allowing us unrestricted access to test this historically overlooked porphyry system.

“Drill results have exceeded expectations, revealing a much larger porphyry system than first recognised, with broad, consistent copper-gold mineralisation extending from shallow depths and largely hidden below shallow gravel cover.

“This discovery has all the signs of becoming our third bulk-tonnage, copper-gold deposit, and is open in all directions and growing fast. We’re also preparing to deploy AI-powered exploration to fast-track our nearby exploration growth pipeline, leveraging 16 years of expertise in Chile.

“With La Verde’s scale potential and the Costa Fuego copper-gold hub expanding, we’re at a major inflection point in Hot Chili’s growth story.”

The project, which hosts the historical La Verde copper mine, is at the core of the historical Domeyko mining district and in the centre of the company’s recently consolidated and larger Domeyko landholding.

La Verde drilling

To date, HCH has drilled 19 holes totalling 5700m at La Verde and received assays from 12 holes.

This has defined a discovery footprint measuring 550m by 400m that remains open in all directions.

Mineralisation starts from shallow depths and extends to more than 300m below surface with indications that its deeper potential remains untapped as eight of the holes reported to date ended in mineralisation.

Adding further interest, the gravel cover at La Verde could mask a much larger porphyry system with the company noting that step-out drilling is now underway.

Drill testing of the historical oxide copper open pit at the project is also pending.

HCH is now awaiting assays from seven additional reverse circulation holes.

It is also planning to carry out diamond drilling to test potential for deeper, higher-grade zones at depth and to test potential for +1km vertical depth extent, typical of other recent major porphyry discoveries, such as the company’s Cortadera discovery and BHP/Lundin Mining’s Filo del Sol find.

Hot Chili’s standout drill intersections raise the mercury at La Verde

December 18, 2024 | Stockhead

- Hot Chili’s thick copper-gold intersections validate historical drilling at its La Verde project

- Second hole’s 308m intersection at 0.5% copper and 0.3g/t gold exceeds expectations

- It also highlights La Verde’s potential to host a higher-grade copper-gold zone

Special Report: Hot Chili’s initial drilling at La Verde has validated its decision to acquire the historical copper mine in Chile after returning thick copper-gold intersections.

While the first hole – DKP001 – provided a good show with a 174m intersection grading 0.4% copper and 0.1g/t gold from 36m, the second hole about 120m to the southeast really upped the ante after recording a 308m interval at 0.5% copper and 0.3g/t gold from a down-hole depth of 46m to the end of hole.

Not only did DKP002 exceed the company’s expectations and end in mineralisation, it also intersected a higher grade zone of 202m at 0.6% copper and 0.3g/t gold from 70m.

The results are hugely encouraging for Hot Chili (ASX:HCH) as the La Verde porphyry footprint measures about 850m by 700m, which is roughly comparable to its higher-grade Cortadera Cuerpo 3 copper-gold porphyry about 30km to the north.

Cuerpo 3 is also the largest porphyry at Cortadera with a higher confidence indicated resource of 798Mt grading 0.45% copper equivalent, or contained metal of 3.6Mt copper and 3Moz gold, and inferred resources of 203Mt at 0.31% CuEq.

What this means is that further drilling successes could unlock another resource of similar size, which will in turn provide a substantial boost to the company’s Costa Fuego copper hub.

La Verde mine

The historical La Verde open pit mine in the Domeyko mining district, which the company acquired in November 2024, was previously exploited by private interests for shallow porphyry copper-style oxide mineralisation with limited drill testing outside the central lease or at depth.

Importantly, it sits in the centre of the company’s recently consolidated and larger Domeyko landholding, secured in an option agreement back in April 2024.

This marks the first time the area has been consolidated, and provides the company with access to a much larger potential porphyry copper deposit footprint measuring around 1.4km by 1.2km.

HCH promptly launched and completed a 12-hole reverse circulation drill program totalling ~3150m with the first two holes designed to validate historical drill intercepts and test the interpreted northern extension of the porphyry from the open pit.

While DKP001 was successful in validating the most notable copper intercept from historical drilling, the assays from DPK002 really demonstrated the value of La Verde by highlighting its potential to host a higher-grade copper-gold zone.

The consistent higher-grade results confirm the extension of the porphyry system almost 400m to the northeast of the open pit, a significant step out considering the existing pit measures about 200m by 400m.

It is also located immediately beneath a gravel cover sequence which obscures the ultimate extent of the porphyry system.

Assays are pending for the remaining 10 holes though the success of the first holes has prompted HCH to expand the RC program by another 2000m of drilling, expected to be completed in late January 2025.

Hot Chili pours new water company into Chilean valley

July 8, 2024 | The West Australian

Hot Chili has entered into a new joint venture (JV) aimed at supplying seawater and desalinated water to mining projects throughout Chile’s Huasco Valley where it is pursuing its own mammoth Costa Fuego copper-gold project.

The company today confirmed it will hold an 80 per cent interest in Huasco Water and its critical water assets in the JV with Chilean iron ore company Compania Minera del Pacifico (CMP). The new company is expected to supply desalinated water to operations including Costa Fuego and CMP’s Los Colorados iron ore mine.

The JV says further offtake negotiations are already underway.

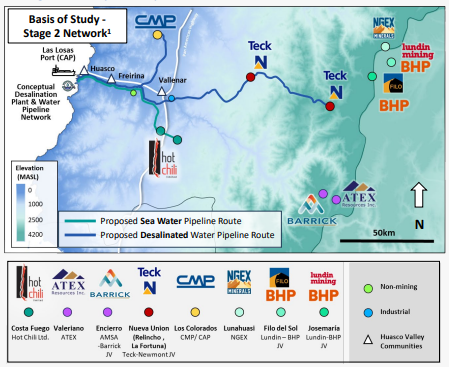

The Huasco Valley region in Chile’s Atacama Desert is one of the driest regions on Earth, inducing significant water demands from mining operations and local communities. The new water initiative reflects an increasing trend in the Atacama region towards collaborative water infrastructure development, highlighted by a recent US$600 million (AU$890 million) deal for Antofagasta Minerals’ Atacama water rights and assets.

The Company has been receiving increasing interest from potential strategic funding parties in its advanced Costa Fuego copper-gold development and its recently announced Water Supply Studies. This interest, in combination with a rising copper price environment, provides confidence to accelerate the Company’s growth and development plans whilst preserving control of these assets.

Hot Chili managing director Christian Easterday

The company holds the only granted maritime water concession and necessary permits to provide critical water access to the Huasco Valley. It has outlined about 3700 litres per second of potential future desalinated water demand from new mine developments around the valley alone.

The JV partners are likely to underpin Huasco Water as potential foundation offtakers with the Costa Fuego copper project requiring some 700 litres per second of future seawater demand, while Los Colorados needs a further 200 litres per second. Hot Chili says significant economic, environmental and social synergies exist for all potential customers in the Huasco Valley, especially given growing community and regulatory opposition to continental water extraction in the Atacama.

Initial offtake discussions are already underway with nearby mine developers, with additional non-mining desalinated water customers expected to come from the area immediately adjacent to the Costa Fuego copper hub.

The Costa Fuego copper-gold project, which lies some 740m up the hill from the proposed Huasco desalination plant, features a measured and indicated resource that sits at 798 million tonnes at 0.45 per cent copper equivalent for 3.62 million tonnes of copper equivalent, containing 2.91 million tonnes of copper, 2.64 million ounces of gold, 12.8 million ounces of silver and 68,100 tonnes of molybdenum. It makes it one of a limited number of “globally-significant” copper developments that are not in the hands of a major mining company.

Hot Chili recently executed a $29.9 million fundraising campaign on the back of a US$15 million (A$22.23 million) net smelter royalty (NSR) deal with Osisko Gold Royalties, aimed at driving its Costa Fuego copper hub in Chile into production. It comes as the red metal’s price recently launched to 60-year highs, prompting majors across the world to look to acquire copper-producing assets of scale.

The Costa Fuego prefeasibility study (PFS) is expected in the second half of this year.

By further securing its water supply and also creating a new company capable of luring significant offtake partnerships, Hot Chili now feels confident enough to sink another 25,000m of drilling into the project. It will also pursue more regional exploration and land consolidation in a show of confidence at the copper project, taking final steps forward before a bankable feasibility study and final investment decision.

Copper, water and deep pockets of cash have Hot Chili set up for an eventful second half of the year. And with copper prices remaining solid, the company appears well-positioned now to give its giant Costa Fuego project a good crack at development.

Hot Chili’s new JV to ensure water supply security for Costa Fuego

July 8, 2024 | STOCKHEAD

- Hot Chili forms water joint venture with Chilean iron ore company Compania Minera del Pacifico

- Huasco Water will develop a multi-user seawater and desalinated water supply network

- This will supply future water demand for communities, agriculture and new mining developments for the Huasco Valley region

Special Report: Water is a valued resource that is scarce in areas like the Atacama, which is why copper-gold developer Hot Chili is pairing up with Chile’s Compania Minera del Pacifico to form a water joint venture.

The Atacama region includes the Atacama Desert – the world’s driest nonpolar desert in the world – and is unsurprisingly one of the most water stressed regions of the world.

It is also where Hot Chili’s (ASX:HCH) Tier-1 Costa Fuego copper-gold project is located – specifically within the Huasco Valley that has a long history of mining.

Costa Fuego includes the outstanding Cortadera deposit with an indicated resource of 798Mt grading 0.45% copper equivalent for contained resources of 2.9Mt copper, 2.6Moz gold, 12.9Moz silver and 68,000t of molybdenum.

Costa Fuego also holds a further inferred resource of 203Mt @ 0.31% copper equivalent for 0.5Mt copper, 0.4Moz gold, 2.4Moz silver and 12,000t molybdenum.

Mines typically need considerable amounts of water to operate, a point highlighted by Hot Chili’s estimate the Huasco Valley may need up to 3,700 litres per second of desalinated water in the future for its new mine developments.

A water supply concept study released in February this year confirmed the potential for a large-scale, multi-user desalinated water network serving the entire Huasco Valley, which rather neatly aligns with the Chilean Government’s push for such networks in the Atacama.

Water supply security

Given how important a secure water supply is to mining developments – including Costa Fuego – agriculture and communities in the Huasco Valley, HCH and Chilean iron ore company Compania Minera del Pacifico have established a new water company HW Aguas para El Huasco SpA (Huasco Water).

The 80-20 joint venture will hold the maritime water extraction licence, water easements, costal land accesses and second maritime application previously held by Sociedad Minera El Águila SpA (SMEA), which is also jointly owned by the two companies.

Huasco Water aims to develop a multi-user seawater and desalinated water supply network to supply future water demand for communities, agriculture and new mining developments for the Huasco Valley region of Chile.

HCH and CMP will be foundation offtakers for Huasco Water with the former’s Costa Fuego project expected to consume some 700l/s of sea water while CMP’s Los Colorados iron ore mine will require about 200l/s of desalinated water.

Water offtake discussions are also underway with nearby mine developers and additional non-mining, desalinated water customers situated close to Costa Fuego.

Water infrastructure trends

The company noted that its approach towards potential outsourcing and development of shared infrastructure, in addition to preserving scarce continental water sources, is fast becoming the accepted and responsible approach for unlocking future mining developments in the world’s most prolific copper producing region.

It highlighted Antofagasta’s recent sale of their water assets and water rights to the Centinela copper mine for US$600 million to a consortium of Transelec and Almar Water, which will finance, build, own and operate an expansion project that will sell seawater to the Centinela mine expansion.

The consortium will build a 144km long seawater pipeline using Centinela’s water rights that will parallel the existing pipeline from port to mine, allowing Antofagasta to save US$380M in capital expenditure for the construction of its stage 2 water infrastructure expansion.

HCH said this highlights the strategic nature and implicit value of critical water access rights within the Atacama, and an increasing trend in Chile towards outsourcing in the industrial infrastructure sector.

Hot Chili to pump in $29.9m to develop Chilean copper play

Hot Chili has loaded its financial base with a $29.9 million fundraising campaign aimed at supercharging its Costa Fuego copper hub in Chile – at a time when the reddish metal’s price is at a 60-year high.

The $119.45 million market-capped company’s significant raise, which it said drew strong demand from Australian and overseas institutional investors, coincides with a rising copper price sitting at about US$4.57 (A$6.91) per pound.

Management says it expects its private $24.9 million placement to be complemented by a further $5 million share purchase plan (SPP) to reach the $29.9 million in new funding. Shares were offered at $1 for both the placement and the SPP.

Following the completion of the raise, Hot Chili says it will move to finish its Costa Fuego prefeasibility study (PFS) in the second half of the year, further secure its water supply and also create a new water company, plug in 25,000m of drilling, pursue more exploration and land consolidation in the next 18 months and kick off a “bankable” feasibility study.

The boost to its finances follows hot on the heels of its recent half-yearly figures that showed it already had A$13.3 million in cash at the bank after reducing its 2024 commitments by US$10 million (A$15.12 million) through consolidating its option agreements, securing its water supplies and filing its technical report for the Costa Fuego copper-gold project.

We control large-scale assets in two of the most critical commodities of our time – copper and water – with two of the most desirable attributes – low-risk and near-term. In combination with a rising copper price which indicates the initial stages of a new copper price cycle driven by lack of supply, this gives the Company confidence to accelerate its growth and development plans while preserving control of these assets for our shareholders.Hot Chili managing director Christian Easterday

Easterday said the company had received increasing interest from potential strategic funding parties to help Costa Fuego’s copper-gold development and its recently-announced water supply studies. He said the project remains one of a limited number of “globally-significant” copper developments that was not in the hands of a major mining company.

Costa Fuego’s measured and indicated resource sits at 798 million tonnes at 0.45 per cent copper equivalent for 3.62 million tonnes of copper equivalent, containing 2.91 million tonnes of copper, 2.64 million ounces of gold, 12.8 million ounces of silver and 68,100 tonnes of molybdenum.

Hot Chili also recently inked a deal with Osisko Gold Royalties, pocketing US$15 million (A$22.68 million) in exchange for a 1 per cent net smelter return (NSR) royalty on copper and a 3 per cent NSR on gold across the Costa Fuego project. Management says the Osisko investment provided an endorsement of its project and its economics from one of North America’s leading royalty-streaming groups.

In addition, the company consolidated its tenure while expanding its ground footprint and kicked off its exploration and resource expansion drilling programs. It updated its resource numbers and obtained results from its initial drilling of its latest satellite targets at Marsellesa, Cordillera and Corroteo, with some good copper hits including 25m grading 0.4 per cent copper from surface with 10m at 0.8 per cent from just 7m depth at Marsellesa.

Hot Chili’s Costa Fuego is a boomer of a resource that is seems to be emerging at just the right time and the latest funding moves look set to put a solid set of wheels under the venture to get it fully on track.

Hot Chili grows Costa Fuego with Domeyko acquisition, where historical copper-gold mines are unexplored at depth

STOCKHEAD

The nearby Domeyko mountains of the Andes in copper-rich Chile. Pic via Getty Images

- Landholding increased by 25% at flagship Costa Fuego project, which has a current resource of 798Mt at 0.45% copper equivalent

- Domeyko concessions bought as exercisable options to purchase for $4m

- Domeyko mining centre hosts several significant historical copper-gold mines, unexplored at depth

Special Report: Porphyry developer Hot Chili has acquired the ‘Domeyko cluster’ tenements to boost the size of its flagship 798Mt Costa Fuego copper-gold project in Chile by 25%.

Costa Fuego has a current resource of 798Mt at 0.45% copper equivalent for 2.9Mt copper, 2.6Moz gold, 12.9Moz silver and 68,000t molybdenum.

Two years of drilling and studies have the project now pegged as a low-risk, low-cost and long-life copper project in the world’s largest producer of the red metal.

Lately, Hot Chili (ASX:HCH) has been busy building out a network around its project with water supply and transport deals in the region.

It’s executed a five-year MoU deal with the nearby port to evaluate bulk tonnage loading alternatives for copper concentrate from Costa Fuego that would include a ‘take or pay volume’ clause based on at least 80% of the project’s future annual concentrate production.

The explorer has also announced a focus on water infrastructure and desalination in Chile’s Atacama region – one of the driest regions on earth.

A new addition to the south

Domeyko is the largest land consolidation undertaken by Hot Chili since Cortadera was added to Costa Fuego in 2019, adding 141km2 and representing a 25% lift in the company’s total tenure in the region.

The move contains several new tenement applications in addition to an option agreement to acquire 100% interest in several key tenements covering a highly prospective, 10km-long copper-gold mineralisation corridor.

The Domeyko mining centre hosts several significant historical copper-gold mines which were principally exploited for oxide mineralisation yet have had very limited exploration for copper sulphide mineralisation.

Both porphyry and structurally hosted styles of mineralisation are present in the area and historic datasets are currently being looked over across several highly prospective targets that have never been drilled.

The total exercisable option to purchase Domeyko comes to $4m, payable within two years to a private Chilean syndicate.

More drilling, exploration and development study workstreams across Costa Fuego are ongoing and further updates on progress of the company’s regional water supply business case study are expected soon.